Section 54F — The 2026 Capital Gains "Shield" for Nagpur Investors

In 2026, capital gains from shares, gold, and commercial assets are rising fast, but so is tax leakage. Section 54F remains one of the most powerful legal routes to preserve wealth by converting taxable gains into residential asset creation in Nagpur.

Section 54F can legally neutralize major capital gains tax liability when structured correctly and executed within timeline rules.

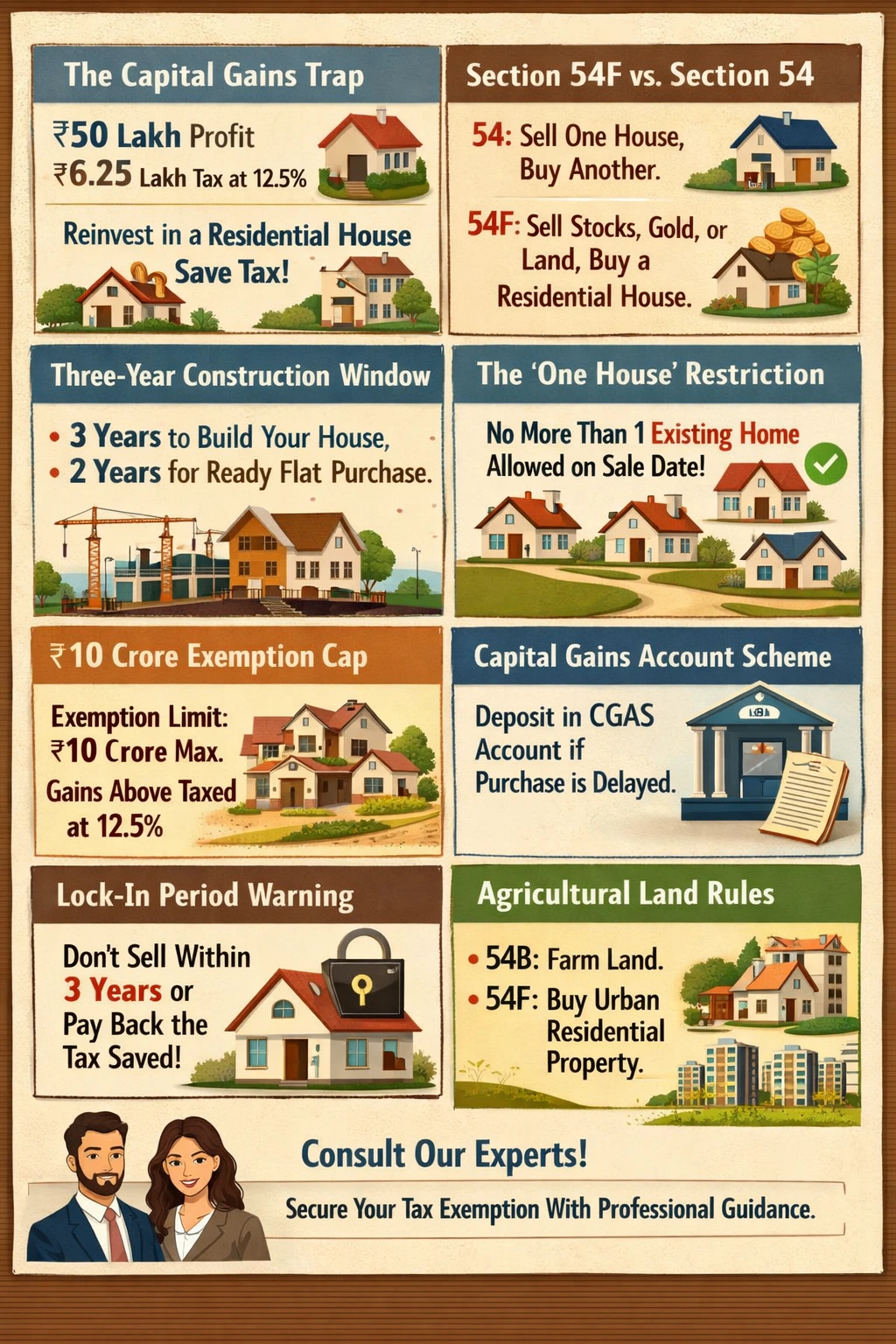

The Capital Gains Trap

With long-term capital gains now taxed at a flat 12.5% post-reform, the effective tax bite on profitable exits has become substantial. If an investor books a ₹50 lakh gain by selling shares or legacy commercial land, the tax outgo can reach ₹6.25 lakh. Section 54F creates a lawful shield by allowing exemption when proceeds are reinvested into a qualifying residential house. For Nagpur investors, this transforms tax burden into asset accumulation.

12.5% LTCG

A ₹50 lakh gain can trigger ₹6.25 lakh tax without a valid exemption path.

54F Objective

Convert taxable gains from non-house assets into residential reinvestment relief.

Understanding Section 54F vs. Section 54

Section 54 generally applies when one residential house is sold and another house is purchased. Section 54F, by contrast, applies when the original asset is not a residential house, such as shares, gold, or certain plots, and the investor buys or constructs a residential property. A critical 54F condition in 2026 is reinvesting net consideration, not merely the gain amount, to maximize full exemption eligibility. This distinction is often the difference between full relief and partial tax liability.

The Three-Year Construction Window

Section 54F is especially useful for plot buyers in growth corridors like Yerla and Shankarpur. The law provides up to three years from original asset sale to complete construction of a residential house. For ready homes, the acquisition timeline is generally two years from sale date. In Nagpur's current execution environment, where approvals and contractor ecosystems are improving, this timeline can be practically manageable when planned early.

The "One House" Restriction

On the date of transfer of the original asset, the claimant should not own more than one residential house other than the new eligible house. This is a compliance-critical condition. Investors who already hold multiple residential units may fail eligibility, even if reinvestment is done correctly. Importantly, ownership of commercial properties or industrial land does not automatically trigger this specific disqualification, but factual review is essential before filing.

"Section 54F is powerful, but procedural precision matters. Timing, ownership status, and documentation discipline determine whether exemption survives scrutiny."

The ₹10 Crore Exemption Cap

Current law places a ₹10 crore ceiling on exemption computation under Sections 54 and 54F. For ultra-high-value transactions, this cap becomes decisive. If gains exceed the eligible cap, only the capped portion can receive exemption treatment and the excess remains taxable at applicable rates. High-net-worth investors moving from commercial exits into premium residential assets in Civil Lines or Ramdaspeth should model this cap before deal execution.

The Capital Gains Account Scheme (CGAS)

When sale timing and property finalization do not align before return-filing deadlines, funds generally need to be parked in a notified Capital Gains Account Scheme to preserve claim continuity. This mechanism demonstrates intent and ring-fences proceeds until eligible purchase or construction is completed. Without timely CGAS compliance where applicable, otherwise valid exemptions can become vulnerable during assessment.

Consequences of "Lock-in" Violation

The newly acquired residential asset comes with a three-year lock-in expectation. Selling too early can trigger withdrawal of earlier exemption and re-taxation in the year of violation, often with additional financial impact depending on assessment outcomes. Investors should therefore treat 54F deployments as medium- to long-term core holdings rather than short-flip inventory.

Agricultural Land Exemptions

Many taxpayers confuse 54F with 54B in agricultural land cases. If agricultural land meeting prescribed usage conditions is sold and another agricultural land is purchased, Section 54B may apply. If proceeds are instead redirected into a residential house, Section 54F logic may become relevant subject to all its conditions. Misclassification can invite defective return flags and follow-up notices, especially under modern automated processing systems.

The Property Bhandar Financial Network

At Property Bhandar, we evaluate every high-value deal through both legal and tax lenses so the asset works not just as real estate, but as a compliant wealth strategy. If you are exiting stocks, gold, or legacy land in 2026, our Tax & Legal advisory desk and empanelled Chartered Accountants can help structure your Section 54F path correctly, from ownership checks to timeline compliance and documentation, so your capital gains shield remains enforceable and audit-ready.

Get 54F Compliance Support